End of Summit

On 11-12 May 2023, Asian Metal held 14th Rare Earth Summit successfully in Ningbo, Zhejiang province. The summit was sponsored by Ningbo Fonne Rare Earth New Materials Co. and contained topics of global rare earth resources, NdFeB magnet, electric vehicle, wind power, automobile louder speaker, motor, hydrogen storage alloy powder etc. The summit was widely supported by rare earth participants, with nearly 200 representatives from home and abroad attending.

The summit started at 9:00 a.m.of 12 May 2023. Mr. Jiawei Jiang, the Content Director of Asian Metal, chaired the summit. Mr. Jiang extended warm welcome and heartfelt thanks to all participants. He mentioned that following the end of the COVID-19, the global commercial intercourse recovered to normal and the rare earth industry entered into a new situation from early 2023. All participants over the world reunited in Ningbo to exchange ideas and share inspiration.

Afterwards, Mr. Xinyi Chen, Deputy General Manager of Ningbo Fonne Rare Earth New Materials Co. delivered the opening speech. He expressed his sincere welcome to participants from all over the world on behalf of Ningbo Fonne Rare Earth New Materials Co. According to Mr. Chen, Ningbo doesn’t have any mineral resources but owns the reputation of “magnet city” as it is one of the major production, innovation and application city of magnetic materials. With the impetus of technical innovation, Fonne maintains long-term cooperation and exchanges with universities and scientific research institutions for experiments and development on new rare earth permanent magnet materials to promote the development of the company and the industry. With strong equipment technology and advanced intelligent automated production process, rare earth metals produced by Fonne owns competitive advantage. Mr. Xinyi Chen also wished the 14th Asian Metal Network International Rare Earth Summit a great success!

Whereafter, Mr. Keyu Song, Senior Engineer of Basic Mineral Strategy Research Office Research Center for Strategy of Global Mineral Resources, CAGS gave a speech on the topic of “Medium and Long-term Supply and Demand Pattern of Rare Earth Resources”. Mr. Song analyzed the rare earth demand trend, rare earth resources supply and forecasted that the supply and demand pattern in the future. According to Mr. Song, rare earth is the foundation of key materials supporting strategic emerging industries as it could be applied in more than 40 industries of more than 10 fields, including aviation, information, electronics, energy, transportation, medical, etc. These downstream applications can be classified to the broad categories of battery alloys, catalysts, ceramic pigments and glazes, glass polishing powders and additives, metallurgy, permanent magnets, phosphors, and other uses. Lanthanum and cerium could be applied into glass ceramics, polishing, lighting, laser, hydrogen storage, petrochemical, metallurgical industry and other fields. Yttrium and europium elements are used in lighting and other fields. Neodymium, praseodymium, dysprosium, terbium and samarium are mainly used in the permanent magnet sector of TV, medical equipment MRI, maglev train, hybrid electric vehicles, military industry and other fields. China has long been the world's largest consumer in this century and its consumption volume in 2022 accounted for 75% of global consumption, with a sharp increase of 10 times from those in 2020. Japan’s rare earth consumption volume reached its peak in 2007 and declined after that. Its consumption accounted the second largest in the world in 2022. U.S.’s rare earth consumption volume hovered at around 10,000t per year over the past years. Following the rapid development of the energy vehicles, wind power generation, artificial intelligence and other related industries as well as the technological revolution of new materials and the continuous expansion of application fields, rare earth demand would increase sharply in the upcoming years.

Afterwards, Mr. Hao Huang, Deputy General Manager of Mianyang GiaStar Magnetic Material Co., introduced the “Sintered NdFeB Magnet Technology Development and Prospects”. He explained the current situation of sintered NdFeB magnet technology. According to him, sintered NdFeB magnet, the third generation of rare earth permanent magnets, also known as the "King of Magnets", is widely used and considered almost irreplaceable in the next three decades. It’s hard to be replaced within 30 years. With its huge advantage in energy density, it plays an increasingly important role in the trend of miniaturization, high performance, and low loss of electrical equipment, and has maintained rapid growth for a long time. In 2021, the global production of sintered NdFeB magnets (calculated as blanks) was around 280,000 tonnes, with output value of more than 100 billion yuan (14.45 billion US dollars). The most conservative estimate is that by 2030, the global demand for sintered NdFeB magnets will reach 500,000 tonnes, with output value exceeding 250 billion yuan (36.12 billion US dollars). NdFeB magnet is widely used in new energy vehicles, traditional vehicles, wind power generation, variable frequency air conditioning, elevator tractors, industrial robots and other fields at present. China saw its new energy vehicle (NEV) market grow rapidly in recent years, with highest growth worldwide for eight consecutive years. In 2022, China’s NEV production and sales reached 7.06 million and 6.89 million units respectively, up by 96.9% and 93.4% YoY. Based on the average consumption of 2.5kg of high-performance NdfeB magnet per NEV,the global demand for high-performance NdFeB is expected to reach 58,000 tonnes in 2025, including 34,000 tonnes from China.

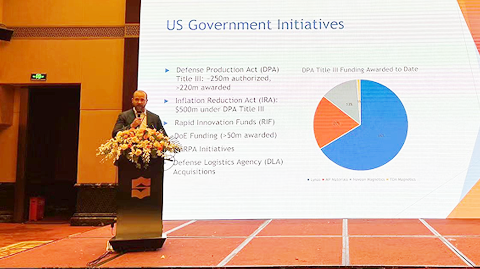

Whereafter, Melvin Hill, Vice President GE Chaplin Inc. shared North American Rare Earth Market Overview and Key Challenges. He disclosed that the current rare earth ore production capacity in America is 43,500t, including 43,000t of bastnaesite and 200t of monazite. American’s rare earth oxide production capacity is less than 300t but it would be enlarged into 35,000t till the end of 2026. US Government recognized critical weaknesses in the domestic rare earth supply chain and has committed significant resources to shore up multiple links in parallel. The robust rare earth concentrate production provides foundation for North American rare earth oxide supply chain, although additional domestic HRE concentrate production is needed in medium term. In the short term, the SEG and heavy rare earth oxide separators lack domestic ore sources jeopardizing supply stability. Light rare earth oxide production capacity will outpace domestic demand in the short and middle term. North American supply chain must look abroad to place new capacity. New demand from North American permanent magnet sector will outpace domestic heavy rare earth oxide supply. Dysprosium and terbium will need to be imported in short to medium term.

After the tea break, Mr. James Lee, CEO of Green Resource Co. delivered a speech on the topic of “South Korean Rare Earth Market”. He claimed that 25.97 million tons of rare earth reserves in Gangwon-do, Chungcheongnam-do, and Ulsan city were identified but with low content of 2.1% and uneconomical. Rare earth reserves in South Korea are not mined and South Korean consumers mainly relies on imported rare earth from Japan, China, U.S. and Russa and other countries at present. Sales of eco-friendly cars have increased rapidly since 2020 due to the promotion of zero-carbon policies by country. Global eco-friendly car production is expected to be about 42.7Mcar as of 2025, which will need toc consume about 64,000t of NdFeB magnet. South Korea began to build their local rare earth metal and NdFeB magnet factories from 2021 in order to meet the climbing NdFeB magnet demand.

Afterwards, Mr. Anton Liu, Global Procurement of Director Harman International Industries, Incorporated gave a presentation regarding “Sustainable Magnet Supply Chain for Automotive Audio”. According to Anton, the car audio market developed rapidly over the past years. Show data showed that the car audio market value already reached about RMB70.7 billion. It would reach about RMB90.5 till 2025. Car audio manufacturers pay attention to intelligent convenience, advanced customization and entertainment. Harman aims to be a best-in-class employer and provider of technology solutions that are beneficial to the long-term wellbeing of the people and communities. Mr. Anton Liu also shared the importance of sustainable magnet supply chain for automotive audio. He disclosed that they try their best to increase the multi-source of NdFeB magnet suppliers in order to maintain the sustainable magnet supply.

Later, Mr. Jingwu Chen, Deputy General Manager and General Manager of Magnetic Application Division Senior Engineer of Earth-Panda Advanced Magnetic Material Co. introduced “Status quo and Prospect for Balanced and Cyclic Utilization Technology of Rare Earth Resources in Rare Earth Permanent Magnet Industry”. According to Mr. Chen, with the highest magnetic performance and the widest application range in current industrial production, rare earth permanent magnet materials can be used in new energy vehicles, intelligent manufacturing equipment, energy-saving household appliances, wind power generation and other fields and are an important foundation for the survival and development of these fields. The output of rare earth permanent magnet materials in China increased from 157,500t in 2017 to 246,000t in 2022, with a compound annual growth rate of 9.35%. The output is expected to continue to grow rapidly in the future, reaching 320,000t by 2025 and over 500,000t by 2030. In 2022, China produced 246,000t of rare earth permanent magnet, including 220,000t of sintered NdFeB magnet, which needs to consume around 66,000t of rare earth metals, including 58,000t of PrNd mischmetal, 4,000t of dysprosium and terbium metal and 4,000t of lanthanum and cerium metals. There is a serious imbalance between the reserves and using volume of rare earth resources, and balanced utilization is necessary.

Afterwards, Mr. Kang Zhong, Executive Director of Ganzhou Fortune Electronics Co. delivered a speech on the topic of “Precious Rare Earths, Valuable Applications, New Applications of High-end Green RE Permanent Magnetic Materials”. Mr. Kang Zhong reviewed the major events of rare earth permanent magnetic material industry over the past years. He also introduced the current distribution of Chinese rare earth resources, the Chinese ionic rare earth industry, the basic and modern technology of NdFeB magnet industry, the current situation and applications of sintered NdFeB magnet. According to him, rare earth industry’s profits are mainly concentrate in the application fields at present. Proportion of added value of rare earth permanent magnet, hydrogen storage material—RE magnetic motor, NI-MH power battery—hybrid electric vehicle is 1:9:16. The It is essential to build a compete industry chain from raw material, intermediate products, downstream applications to recycling in order to reflect the real value of rare earth.

Whereafter, Mr. Wayne Park GM of Sales &Marketing Lynas Rare Earths gave a speech on “Performance of Lynas and PrNd Market Balance”. According to Mr. Park, Lynas can stably produce 600 tons of PrNd per month if no external interruptions such as water shortage, chemical reagents supply, electricity shutdown. In Q1 of 2023,Lynas produced 1,724t of PrNd, which accounted 40% of their total production, up by 14.23% QoQ. Lynas Malaysia’s operating license was renewed for 3 years from 3 March 2023, with no change to the conditions prohibiting the import and processing of lanthanide concentrate after 1 July 2023. If not removed, these conditions will require the closure of the Lynas Malaysia cracking and leaching plant from 1 July 2023. Lynas is pursuing legal and administrative appeals against these conditions. Rare earths are essential to the global energy transition. The production of per 10 million battery electric vehicles and hybrid electric vehicle needs to consume more than 7,000t and 5,000t of PrNd oxide respectively. The production of per 10GW capacity direct drive wind turbine requires 3,000t of PrNd oxide. He forecasted that rare earth demand from electric vehicles and wind turbine industries would keep climbing in the coming years. According to his prediction, the output of electric vehicles would grow fast with about 12% annual growth in average in the coming years. He noticed that wind turbine installation plan shows strong growth as well, especially annual growth rate of off-shore Wind farm projects would reach over 33% in coming 5 years. Lynas has ramping up plan to support PrNd demand growth especially in EU and US.

Afterwards, Mr. Jinyu Li, Chief Engineer of XTC Hydrogen Energy Science and Technology (Xiamen) shared the “Rare Earth Hydrogen Storage Alloy Industry Current Situation & Development Trend”. According to Mr. Li, the well proven commercial application for rare earth hydrogen storage alloy is hydrogen storage alloy LaNi5 (AB5 type) and hydrogen storage alloy La-Mg-Ni (A2B7 type) in the Ni-MH battery industry. Hydrogen storage plays a key role in hydrogen energy development and rare earth hydrogen storage is one of the most promising hydrogen storage technologies. Significant cost reduction will be achieved through replacement of low-cost lanthanum and cerium for mixed rare earth, representing rational utilization of rare earth resource and motivation to push forward sustainable rare earth development. China has many producers of hydrogen storage alloy with a total production capacity of more than 250,000t, bringing excess capacity. There are only three producers of hydrogen storage alloy in Japan, with a production capacity of more than 3,000t each contributing to a total capacity of about 15,000t. The capacity utilization rate is high. China’s annual sales of rare earth hydrogen storage materials basically maintain at 9,000t since 2011. Rapid market development of Toyota Ni-MH mix-power vehicles pushed forward the growth of alloy powder market in the recent years. The market of in-car backup power (e-call, T-box), rail traffic backup power and energy-storage backup power has enormous development potential, and Ni-MH battery has great advantages in the broad-temperature discharging field with a rather promising future.

After the tea break, Mr. Ale? Leben, Managing Director for Asia Business of Domel d. o. o. analyzed “The Supply and Demand of Motors”. His report contains complex 3D designs & optimization, design & advantages, rare earth raw material price trends forecast and short introduction of Domel d. o. o. According to Mr. Ale? Leben, the distribution of global brushless DC motors for gardening equipment and powder tool are 36.5%, 26%, 18.5%, 7% and 12% for North America, Europe, Asia-Pacific, South America, middle East & Africa. The global automobile pump market value reached USD14.17 billion in 2021. The value is expected to increase with a compound annual growth rate of around 4.3% from 2023 till 2030.

Whereafter, Ms. Yan Guo, Deputy General Manager of NingBo NingGang Permanent Magnetic Materials Co. shared a report on SmCo Magnet Industry Status and Outlook. SmCo magnets are primarily made from samarium, cobalt and other metal materials through proportioning, smelting into an alloy, and then crushed, pressed, and sintered. Owing to its excellent magnetic properties, SmCo magnet has partially replaced AlNiCo magnet. To date, rare earth permanent magnets have experienced the first generation of SmCo5, the second generation of precipitation-hardened Sm2Co17, and the third generation of NdFeB magnets. Global production of SmCo magnets is about 5,000t per year. There are nearly 30 producers in China, mainly in Zhejiang and Sichuan provinces, with total annual production of around 4,000t and about 10 producers outside China with annual output of around 1,000t. From a global perspective, foreign countries remains ahead of China in overall SmCo magnets technology and performance, including pressing technology, product performance consistency and mechanical strength, etc. The development of emerging application markets, such as automotive electronics (especially NEVs), 4C integration, 5G communications, high-speed motors (including traction motors for rail transit) and motors used by the energy storage industry is expected to bring more new opportunities to the SmCo magnet industry. However, the current production capacity can already meet market demand for expansion.

The following changes are expected in the next few years for SmCo magnets: With the fierce competition of SmCo magnets gradually shifting to the stage of reducing capacity, destocking, cutting costs and making up for shortcomings, the low-end market will face intensifying competition in the next few years as lower profit margin might lead to losses. In the end, a small number of enterprises with capital, scale, technology and market advantages will remain to occupy the relevant market.

The last speaker of the summit was Mr. Jianping Liu, General Manager of Ganzhou Shi Lei Rare Earth Materials Co. His topic was “Status Quo and Outlook of Rare Earth Fluoride”. According to Mr. Jianping Liu, rare earth fluoride, also known as rare earth fluoride. refers to 17 kinds of rare earth element fluorides with atomic number from 57 to 71, and scandium and yttrium with atomic number from 21 to 39. It is generally in the form of gray powder, insoluble in water, easily soluble in acid, and chemically stable. It were mainly applied in electrolysis and reduction of rare earth metals, special glass, Grain boundary diffusion, ceramic and functional materials. More smelters set up their rare earth fluoride production lines in order to improve the industrial chain, including 2 smelters in Jiangxi, 2 smelters in Fujian, 1 smelter in Guangxi, 2 smelters in Shandong and many smelters in Baotou. He disclosed that continuous and specialized production through dry method can improve the output of a single fluorination equipment, reduce energy consumption and labor costs, and improve the level of enterprise management. He suggested that enterprises that have the conditions to handle the comprehensive utilization of fluoride and chloride ions can open up wet production to reduce production costs. Enterprises that require dry production of high priced, high-purity medium to heavy rare earths (terbium, dysprosium, holmium, erbium, gadolinium, yttrium) can choose their own fluorination process based on actual application scenarios, and dry production is advocated. He appealed enterprises to improve the smelting process and metal quality, to constantly promote the application of functional materials in high-end fields. He called on rare earth participants to make unremitting efforts for China’s science and technology developments.

At 18: 00 p.m. of 12 May 2023, the banquet started and Ms. Lujing Zou, Executive Vice President of Ningbo Fonne Rare Earth New Materials Co. delivered welcome speech. Ms. Lujing Zou welcomed all participants to come to Ningbo and shared her prospect forecast as well expressed her best wishes to rare earth industry. The dinner was full of happiness and joy. Following with the joy and laughter, Asian Metal’s the 14th Rare Earth Summit closed smoothly with the great support from sponsors, speakers and participants. Asian Metal has successfully held rare earth summits over the past years, which received great support and cooperation from market insiders. Sincere thanks to you! Asian Metal will continue to march forward with professional spirit and provide timely and accurate market information about metals for participants. Let’s meet in the 15th Rare Earth Summit!